Best bank for travelers and digital nomads: multiple currencies in one account!

It’s not Charles Schwab nor Citibank. This best bank for travelers that I am talking about can handle up to 10 currencies at the same time and transfers are real-time too! The currency conversion is way better as well!

Reader mail: Hello Trisha. I’ve been following you for a while on Instagram and your blog. I am amazed by all your travel stories! I am a follower since your South America days in 2013. I was always curious about how you manage finances. What is the best bank for travelers in your opinion? I am going on a backpacking trip soon and I want to see how you do it since you are always moving around different countries. Thank you in advance and keep up the great content!

– Stanley Pucci, USA

Hi Stanley!

Thank you for your message and thanks for following the blog! I don’t think a lot of people know that handling your finances as a digital nomad is super hard. I was just talking about this to a friend today. It’s really not that easy, especially if you’re moving around constantly.

It took me years to finally find the best bank for travelers and I’d love to share this journey with you. If you have any questions that weren’t answered in this post, feel free to get in touch with me anytime!

Good luck and I hope this helps!

Xx,

Trisha

I’ve been traveling full-time for the past 10 years, without going back home to the Philippines. You can imagine how tedious that process is if you are a Philippine bank account holder. I experienced a lot of inconveniences. In 2014, for the first time in my life, I was robbed in Rio de Janeiro. Don’t worry, nothing bad happened to me. You can read that story later.

Every ATM card that I have was in that wallet. When I was younger and was beginning to travel, I made sure I had all the ATM cards in every major bank in the Philippines: BPI, BDO, Metrobank, and Unionbank. If you come to think of it, having all these accounts does not make sense. More on that later but I’d like to explain to you the hassle I went through when my wallet got stolen in Rio de Janeiro.

Related: The cost of living in Puerto Vallarta, Mexico

The time difference between the Philippines and Brazil is 14 hours, the Philippines being ahead. I lost my wallet at 14:00 so that was 4:00 in the morning in the Philippines. There was no way that anyone in the banks can assist me. All I wanted to do was cancel the cards and for them to send me a new one.

I waited for a little bit to call the bank. When I reported my case and asked them for a new bank account, they told me that they cannot send me a bank card in Brazil, that the Philippines do not do those kinds of things. They can only send it within the Philippines is what they said. From this moment, I realized how bad bank security in the Philippines is.

All over Europe and probably most first-world countries can send bank cards abroad. For example, when my Croatian friend lost his bank card in Ecuador, he called his bank and within 4 days, the card was in his hands. The bank directly sent it to him!

The same goes for my French and American friends. They would even send it to your hostel which I found a little bit extreme: how do European and American banks trust these addresses? Why would they send a bank card to a hostel?

Then I realized it’s just really a matter of security. Every country has higher bank security than the other and unfortunately, in the Philippines, we do not have that high-end system.

So what I did was very very very tedious. I wrote an authorization letter so that my mom can take the bank card for me. I signed it and sent it. My mom went to the bank to retrieve my new bank card and they told her that my authorization letter should be sealed by the Embassy of the Philippines in the country I was in (Brazil).

So, I did that too. It was tedious! When my mom got the bank card, she sent it to me. And sending a package from the Philippines to Brazil is rather costly. She paid about $200 USD just to send me a bank card.

But I want to clarify that this happened years ago. I am not sure if they are asking for the same requirement now. Probably, this will be irrelevant to you as you read through this post, you will realize how inconvenient Philippine banks are and you’ll probably stick to my recommendation of the best bank for travelers.

Read on…

Why I gave up on local banks

Aside from the inefficiency, poor service, or crazy timezone difference, there are a lot of reasons why I just gave up on Philippine banks. The interface of both mobile and online banking is so not user-friendly to me.

The technology is really bad and there’s always that annoying option for travelers where the banks send one-time passwords (OTPs). As the years go by and I never get to go back to the countries where I have local bank accounts, I lost track of what mobile number I used in registering for my online access.

That was another cross mark on my efficiency list. Do I need to go home all the way from South America to change a mobile number? Of course, not. And I won’t. They won’t even accept it if you do it by phone!

See also: How to open a bank in Mexico as an expat or a tourist

OTPs are standard to all banks, hence, you always have to have an active mobile number. At the time, I was just hopping from Argentina, Peru, Brazil, Uruguay, etc so I was frequently changing sim cards. Now that I am more stable in Mexico, I only have one sim card.

Remember that I may have found the best bank for travelers but an active mobile number is still necessary. It’s just easier for me to keep one now since I am just in Mexico. I haven’t moved for the last 2 years.

Having multiple bank accounts in different countries: does it make sense? Today, you can now do inter-bank deposits but when I started traveling, you can only do deposits to the same bank. This is the reason why I had all these 4 bank accounts which were totally unnecessary.

The international wiring fees are insane, too! As a digital nomad, I manage different currencies so local banks are a no-no.

Paypal? I gave up on that too

For many freelancers, Paypal has been very common and efficient. Imagine, if you are a digital nomad and your client/employer is in the USA or Europe, how will they pay you?

But the conversion is sh&t. I feel like Paypal earned a lot from me just by their transfer commissions. And what I hate the most about Paypal is their country limit. Sure, you can add different currencies within your Paypal account but you can only add Philippine bank accounts because you are from the Philippines. The same goes for all nationalities. You can never add multiple bank accounts from different countries in one Paypal account.

Which sucked because of my set-up: I earn in USD. When a client sends me USD through Paypal, he’s charged a commission and I am too. But this only happens if your Paypal accounts are from different countries.

For example, if it’s PH to PH, there will be no fees for both parties. If come to think of it, I just get charged $4 USD per transaction but if you look at the entirety of it, especially for a digital nomad like me who has lots of Paypal activities, I’ve come to realize that I’ve reached at least $2,000 USD in fees through the years.

What also sucks is that I had a Paypal in Spain (EUR) and a USA Paypal account. It’s just a lot of accounts to manage!

Paypal’s interface is surely user-friendly and transferring money to your Philippine bank account entails easy steps. Sure, it’s familiar. But the more you get comfortable with it, the more you don’t check the conversion rate that you will receive. You are only eager to transfer the money so you can have it immediately.

But if you take a second look at Paypal’s conversions, they are way way way way way low. And I find it really unfair!

Not only that, since you have a Philippine Paypal account and you receive USD, the USD you transferred will then be converted to Philippine peso. Conversion rates change daily but if you check Google right now, for example, USD to Philippine peso, it will show you 48 pesos but Paypal will just give you between 43-45 pesos. And that’s a lot! You might think it’s just 3 pesos but we are talking about conversion from each dollar. Do the math!

Then another conversion happens if you withdraw it in Brazil, Mexico, or whatever country you are in. Not to mention the withdrawal fees that these countries are charging which are usually $2-$5 USD depending on the country. In short, your money gets converted three times and that never looks good.

Again, do the math. I did and it made me tired. It made me feel like I wasn’t really getting the money I worked hard for. And so, I quit Paypal, too.

Wise: the best bank for travelers

And the best bank for travelers is… WISE!

It’s not Citibank, not Charles Schwab (that’s why I closed this US account too). It’s WISE!

I am totally in love with Wise because it has great conversion rates and it gives you a personalized bank account for every country in the world! Right now, I have USA, Australia, Singapore, United Kingdom, and European bank accounts in one!

I said goodbye to 4 multiple bank accounts in different countries because it really did not make sense. Wise is a gem and it is truly the new way of managing your money all over the world.

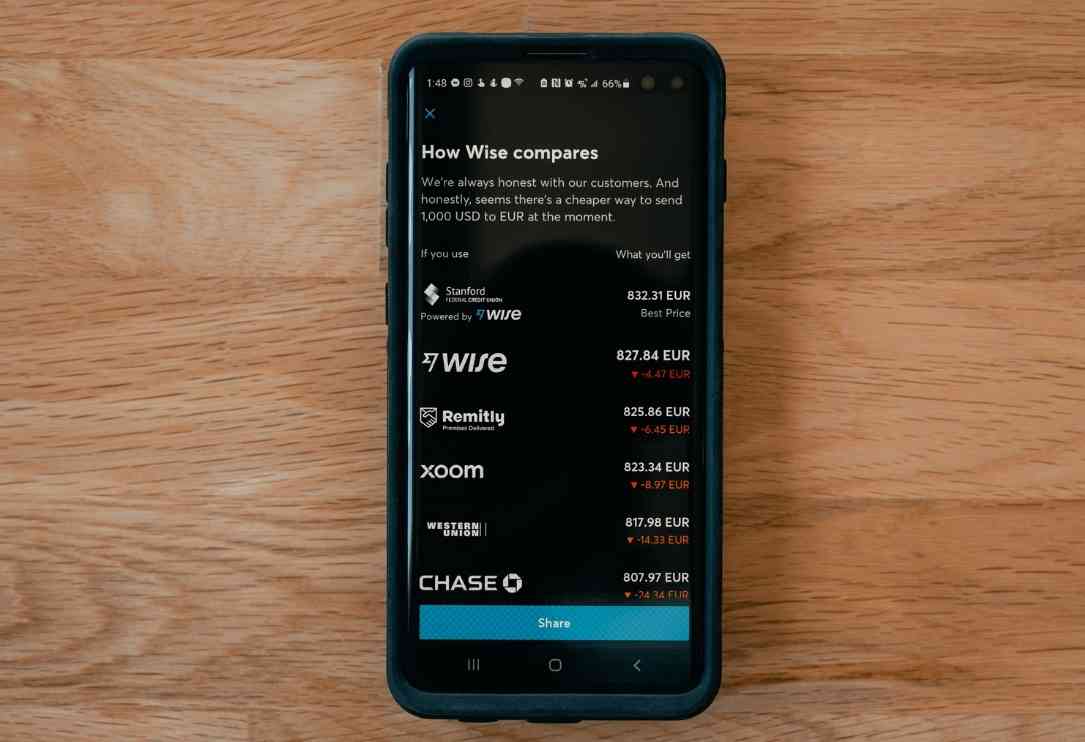

Their fees are super high! Well, I say super high now because I was really shocked and discouraged by Paypal’s conversion rates. Wise’s rates are always fair and more often higher than any bank in the world.

I am not sure how they are able to do this but this is amazing that one company actually cares for its customers. For example, I checked USD to Mexican peso today. Paypal says $18.50 for every dollar. Google says $21.72 and Wise? $21!

I always trust Google’s conversion because I feel like it’s the worldwide conversion but look at the difference between Google and Wise. You will see how low their commission rates are!

☕ Support this blog’s honest and transparent journalism. Help us add value to our content! Keep P.S. I’m On My Way content free for all by donating to our coffee fund.

Signing up for a Wise account

Step 1: Go to the Wise website

Choose “personal” account. It will ask you for your email address, password, and country of residence. I put the Philippines as my country of residence since I still don’t have residency in another country. I am just a traveler. It will also suggest that you sign up with Google, Facebook, and Apple.

I chose “Apple” so the app will trust my phone whenever I want to access it. Once you fill out these easy items, you will receive an e-mail from Wise asking you to confirm your e-mail address. Confirm the e-mail and you’re good to go!

Step 2: Fill out your personal details

Just some basic stuff like full name, address, etc. Remember that this information will not affect any of your multi-currency bank accounts with Wise. They are only asking for this for identity verification. Always put your legal name, as seen in a legal ID.

Step 3: Get started with balances

In this section, you will select all the currencies that you want to open. In my case, I have a USA, United Kingdom, Europe, Australia, and Singapore. This way, I can always receive money from different clients all over the world.

You’ll always want your clients to have options to transfer to a bank account. I once opened a Japanese bank account in my Wise balances just because I had a campaign in Japan and it was way easier for them to do bank transfers.

You can always close your currencies but it is also good to know that you can also always open a new one without limit. The bank accounts are generated automatically so it only takes seconds for you to open a bank account in different countries with Wise.

For real, they have bank account digits, routing number, IBAN/BIC, and all the bank details you will need without having to physically go to a bank to apply!

![]()

After this, you can start receiving payments by sending your bank details to your clients all over the globe. The transfer is always instant in my case! I even added my US bank account on Wise to my Airbnb payouts (I’m an Airbnb host, remember?) and it always works smoothly! It’s always good to receive USD to USD! I feel so happy about using Wise!

Best bank for travelers FAQs

I’m sure you’ll get a hold of the app or Transferwise’s website interface once you explore it. It’s a new trend but it’s really easy to understand. I’d like to share with you some of the frequently asked questions I receive from readers.

How do you actually withdraw money after you receive them?

Wise has its border-free cards which can also be used as debit cards but they only have them in the USA, Europe, Australia, and some parts of Asia. It is not worldwide yet. Better check if Wise debit cards are available in your country. Wise debit cards also follow their own conversion rate so you won’t lose a lot of money from conversions!

What if my employer/client asks me for a bank name?

Sure, on the TW app, you will only see account numbers but you cannot actually see a bank name. All you have to do is to click on the blue rounded question mark below the address which you will find at the end of every bank account detail.

Wise provides all bank partners they have in each country. What’s best about this is that they only partner with one bank per country so it is 100% guaranteed that your bank account is actually registered in a bank somewhere.

I have been using Wise for years and it makes life so much easier. I’m from the US but I’ve been living in Spain for 5 years. I’m not a digital nomad though, so I only have to deal with two countries. I did need to open a Spanish bank account for my job, so I did that when I moved here 5 years ago. I have paypal connected to my US bank account and then I use Wise to move money between the two! It’s so easy! I also have an account on there like you do, but I don’t have as much of a use for it as you do.

I do so much banking online I hadn’t thought about how to handle having replacement cards sent abroad and it would never have occurred to me that a bank would say no. That could create some chaos for sure. And I hate fees so PayPal would be a definite no for me. This is the first I have heard of WISE and can’t imagine why everyone isn’t using it. The company has absolutely found unfilled nitch!

I love the idea of a bank account that can handle multiple currencies. We have paid far too much in foreign transaction fees. Sadly Canadian banks and credit cards sometimes are not recognized everywhere we travel. So we are always looking for options. I may have to take a close look at WISE.

WISE sounds good and it’s easy to open an account. I must check this out and learn more about it. I wonder if someone from Indonesia can transfer money to my WISE if I have an account. It will be fast and more safe, I believe.

This is a much-needed suggestion for me. I am so tired of Paypal and those services. The conversion rates and the prices are too high. I must check how this works for me with INR. Thanks for the suggestion

Thanks for introducing me to this bank. Being a traveler that I am, I like banks that handle multiple currencies and it is amazing to know that Wise can handle 10 currencies at a time. So cool! I think it is important to choose the right bank while traveling so we don’t get charged unnecessary charges.

I can totally understand the problem with PayPal! Their conversion rates are really a pain. And my country has a host of rules for Paypal! The concept of one bank for travellers is quite lucrative and I would definitely like to check out on Wise. It sounds good and the process of opening an account also seems easy.

Thanks for letting me know about Wise. I used to be worried about losing my actual wallet or being robbed while travelling to some part of the world. Plus I am not so into Paypal or the local banks. So Wise looks to be a great helpful aide.

Hi Trisha, recently subscribed to your blog (which I rarely do). Question – I have a 4 year temp residency visa in Mexico. I am opening an LLC in USA and a USA bank account also.

My official residency is Australia but I will not be returning (and my Aussie drivers licence ID has just expired) and so I want to start building a profile outside of Australia.

I now have a Mexican Drivers Licence. I would like to state that my residency is Mexico (as I have a 4 year temp residency permit) but it looks like I will not receive a debit card from wise if I do (based on my understanding of this article).

What do you suggest if I want to receive a physical debit card from Wise and I want to avoid categorising myself as a resident of Australia.